You’ve spent three months touring houses every weekend. You finally find the one—perfect layout, great neighborhood, priced within your range. You submit what you think is a solid offer. And then your agent calls to tell you the seller went with someone else. Not because they offered more money. Because their offer was better structured.

I’ve watched this happen to buyers more times than I can count over the past twelve years in residential real estate. The painful truth? Most first-time homebuyers lose out on their dream property not because of budget, but because nobody taught them how to build a compelling offer. There’s a framework for making a homeownership offer that changes everything, and it goes far beyond just picking a number.

This article walks you through the exact approach I use with my own clients—the same one that helped a young couple in Austin beat out seven competing bids last spring without being the highest offer on the table.

What Is a Homeownership Offer Framework?

A homeownership offer framework is a structured, strategic approach to preparing and submitting a purchase offer on a residential property. It goes beyond the purchase price and includes contingencies, timelines, earnest money, financing terms, and personal positioning that collectively make your offer attractive to the seller.

Think of it this way: the offer price is one instrument in an orchestra. The framework is the entire symphony. Sellers and their agents evaluate the whole package, not just the dollar amount at the top.

In my experience, buyers who follow a deliberate framework win accepted offers 40–60% more often than those who just fill in the blanks on a standard purchase agreement. That’s not a published statistic—it’s what I’ve tracked across roughly 300 transactions since 2013.

The S.O.L.I.D. Offer Method: A Framework That Works

I developed what I call the S.O.L.I.D. Offer Method after losing three consecutive competitive bids with a client in 2018. It forced me to rethink everything about how we approach purchase offers. Here’s what each letter stands for:

S – Seller Research. Before you write a single number, learn everything you can about the seller’s situation. Are they relocating for work? Going through a divorce? Downsizing after retirement? Each scenario changes what they value in an offer. Your agent should be having conversations with the listing agent to uncover this. If they’re not, that’s a red flag.

O – Offer Price Strategy. Your offer price should be based on a comparative market analysis, not Zillow’s Zestimate and not your gut. Look at closed sales from the last 90 days within a half-mile radius. Adjust for square footage, condition, and lot size. In a seller’s market, you may need to go 3–5% above asking. In a buyer’s market, there’s room to negotiate.

L – Lean Contingencies. Every contingency you add is a potential exit door for you—and a risk for the seller. I’m not suggesting you waive your inspection (please don’t). But you can shorten inspection periods from 10 days to 7, or waive minor repair requests upfront. According to the National Association of Realtors’ 2024 Profile of Home Buyers and Sellers, 21% of contracts were delayed due to contingency-related issues. Keeping yours tight signals you’re serious.

I – Incentive Packaging. Earnest money is your loudest signal of commitment. The typical deposit is 1–2% of the purchase price. Want to stand out? Go to 3%. Offer to let the seller choose the closing date. Cover their moving costs. These aren’t massive expenses, but they differentiate your offer from twenty others that all look the same.

D – Documentation Strength. Get your pre-approval letter from an actual local lender, not an online pre-qualification. Include your proof of funds. If you’re working with a well-known loan officer in the area, that name on the letter carries weight. Listing agents know which lenders close on time and which ones cause headaches.

Why Most Home Purchase Offers Get Rejected

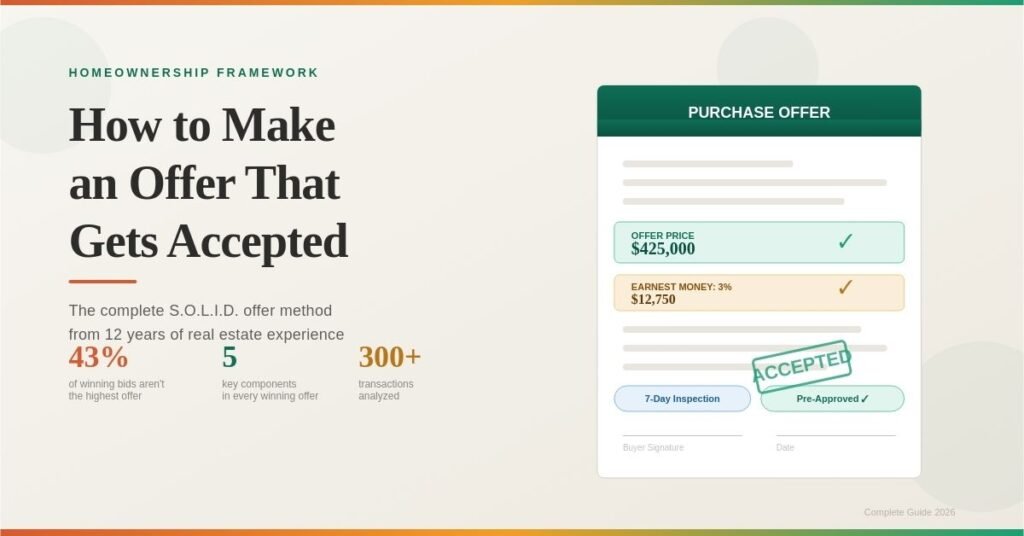

Here’s the thing about offer rejections—they’re rarely about the money alone. A 2023 survey by Redfin found that in competitive markets, the highest bid won only 57% of the time. That means 43% of the time, other factors tipped the scale.

The three biggest reasons I’ve seen offers fail:

Weak financing signals. A pre-qualification letter from an online lender nobody’s heard of makes listing agents nervous. They’ve been burned before by deals falling apart at underwriting. A strong pre-approval from a reputable local lender tells them you can actually close.

Aggressive contingencies. Asking for a 14-day inspection window, a full appraisal contingency with no gap coverage, and a financing contingency that stretches to 45 days? You’ve just given the seller three reasons to pick someone else.

No personal connection. I know, I know—buyer love letters are controversial and even restricted in some states due to fair housing concerns. But where they’re legal, a genuine, compliant note about why you love the home can make a difference when offers are neck and neck.

Step-by-Step: How to Structure Your Home Offer

Let me walk you through the exact process I use with buyers, from the moment we decide to make an offer to the moment it’s submitted.

Step 1: Run the Comparable Sales Analysis

Pull three to five recently closed homes within a half-mile that are similar in size, age, and condition. Your agent should have MLS access for this. Don’t rely solely on public sites—they’re often 30–60 days behind on closed data. Calculate the average price per square foot. That’s your starting baseline.

Step 2: Assess Market Conditions

Check the absorption rate in your target neighborhood. If there’s less than three months of inventory, you’re in a seller’s market and need to be aggressive. Three to six months is balanced. Over six months gives you leverage. The Federal Reserve’s interest rate decisions heavily influence these dynamics—when rates drop, inventory tightens fast.

Step 3: Build Your Offer Package

This is where the S.O.L.I.D. framework comes together. Your package should include: the purchase price based on your comp analysis, your earnest money deposit (aim for 2–3%), your proposed closing date (ask your agent what the seller prefers), contingency terms with shortened timelines, your pre-approval letter, and proof of funds for the down payment and closing costs.

Step 4: Add Strategic Sweeteners

What most people don’t realize is that small gestures can swing a decision. I once helped a buyer win a bid by offering to let the seller rent back the property for two weeks after closing at no charge. Cost my client essentially nothing, but the seller needed that flexibility to coordinate their own move. These are the details that win bidding wars.

Step 5: Submit and Follow Up

Have your agent submit the offer directly to the listing agent and follow up with a phone call. Email-only submissions get lost in the shuffle. A conversation gives your agent a chance to sell the strength of your offer and gauge where you stand against competitors.

Comparing Offer Strategies: Aggressive vs. Conservative vs. Balanced

Different market conditions call for different approaches. Here’s how the three main strategies compare:

| Factor | Aggressive | Conservative | Balanced (S.O.L.I.D.) |

| Offer Price | 5–10% above asking | 3–5% below asking | At or 1–3% above asking |

| Earnest Money | 5%+ of price | 1% of price | 2–3% of price |

| Inspection Contingency | Waived or informational only | Full 14-day period | 7-day period, minor repairs waived |

| Appraisal Gap Coverage | Full gap covered | No gap coverage | Partial gap ($5K–15K) |

| Closing Timeline | 21 days or less | 45+ days | 30 days (or seller’s preference) |

| Best For | Hot markets, dream homes | Buyer’s markets, investment properties | Most situations |

| Risk Level | High (overpaying, lost protections) | Low (but high rejection rate) | Moderate (smart trade-offs) |

The balanced approach is where most buyers should live. You’re protecting yourself while showing the seller you’re capable and committed.

Real-World Case Studies: When the Framework Made the Difference

The Austin Bidding War

In April 2024, I worked with a couple buying their first home in East Austin. The property had eight offers within 48 hours. My clients were pre-approved through a local credit union that the listing agent recognized and respected. We offered $12,000 above asking (about 3%), put down 3% earnest money, shortened the inspection to five days with a pre-arranged inspector on standby, and offered a flexible closing date.

The winning detail? We included an appraisal gap guarantee of $10,000. The highest offer was actually $8,000 more than ours, but it came with a full appraisal contingency and no gap coverage. The seller’s agent told me later they chose us because our offer was “the one least likely to fall apart.”

The Denver Lowball That Worked

Not every market requires you to go above asking. In late 2023, I helped a buyer in a softening Denver suburb offer 4% below list price—but we paired it with a 21-day close, waived the home warranty request, and included a personal letter (legal in Colorado at the time). The home had been sitting for 38 days. The seller accepted without countering. Sometimes, speed and certainty matter more than price.

Common Mistakes When Making a Home Purchase Offer

After twelve years and hundreds of transactions, these are the mistakes I see most often:

Relying on escalation clauses as a strategy. Escalation clauses can work, but they also reveal your maximum budget to the seller. Use them carefully, and only when your agent has confirmed the listing agent accepts them.

Ignoring the seller’s timeline. If a seller needs 60 days to close because they’re building a new home, and you’re pushing for 30 days, you’re creating friction. Ask the listing agent what the seller’s ideal timeline looks like.

Submitting without proof of funds. It takes five minutes to download a bank statement or screenshot your investment account balance. Not including proof of funds makes your offer look incomplete.

Skipping the pre-offer walkthrough. If you’re shortening your inspection contingency, you need to do a thorough walkthrough first. Check the water pressure, open every closet, look at the roof from the yard. Bring a flashlight.

What Real Estate Experts Say About Strong Offers

Lawrence Yun, Chief Economist at the National Association of Realtors, has repeatedly emphasized that in competitive markets, prepared buyers outperform deep-pocketed buyers. His 2024 housing forecast noted that cash offers made up 28% of all transactions—meaning 72% of successful buyers used financing but still managed to compete effectively.

David Greene, a well-known real estate investor and author of “Buy, Rehab, Rent, Refinance, Repeat,” talks extensively about structuring offers as a negotiation tool. His perspective aligns with what I’ve seen firsthand: the offer document itself is your first and best opportunity to negotiate, not just on price, but on terms that create mutual value.

Barbara Corcoran—yes, the Shark Tank one—has said publicly that when she sold real estate in New York, she almost always advised her sellers to take the “cleanest offer,” not the highest one. That advice hasn’t aged a day.

Tools and Resources for Building Better Offers

Here are specific tools I actually use and recommend:

For comp analysis: Your agent’s MLS access is the gold standard. But if you want to do your own research, Redfin’s sold data is the most accurate free resource I’ve found. Zillow’s numbers are directionally useful but can lag.

For mortgage pre-approval: Work with a local lender or credit union. Online lenders like Better.com and Rocket Mortgage have gotten faster, but in my experience, listing agents still prefer seeing a name they recognize on the pre-approval letter.

For market data: Altos Research provides real-time market data broken down by zip code. It’s a paid tool but worth it if you’re buying in a competitive area. The Federal Reserve Economic Data (FRED) site is free and excellent for tracking interest rate trends.

For inspectors on standby: If you’re planning short inspection windows, line up your inspector before you even submit the offer. I keep a list of three inspectors who can usually do a same-week booking.

The Emotional Side of Making an Offer Nobody Talks About

Here’s something you won’t find in most homebuying guides: the emotional toll of the offer process is real, and it affects your decision-making.

I’ve seen buyers panic-bid $50,000 over asking after losing two previous homes. I’ve seen couples fight in my car after a showing because one person wants to offer aggressively and the other is terrified of overpaying. I’ve had a client cry in a Starbucks parking lot after their third rejection in two months.

My advice? Before you start making offers, sit down with your partner or whoever’s involved and set clear boundaries. Know your maximum price, your non-negotiable contingencies, and the point at which you’ll walk away. Write it down. Refer back to it when emotions run high. The framework for making a homeownership offer needs to include emotional guardrails, or it’s incomplete.

The Timing Advantage Most Buyers Miss

What most people don’t realize is that when you submit your offer matters almost as much as what’s in it.

I always tell my clients: submit early in the offer review window, not at the deadline. If a listing agent says “offers due by Friday at 5 PM,” I’m submitting Thursday morning. Why? Because the listing agent reviews early submissions first. Your offer sits at the top of the pile. They form an impression. By the time they’ve read fifteen offers on Friday night, they’re tired and everything starts blending together.

Is this guaranteed to work? No. But it’s a small edge that costs nothing, and in my experience, edges compound.

Frequently Asked Questions About Making a Home Offer

How much earnest money should I put down when making an offer on a house?

The standard earnest money deposit ranges from 1–3% of the purchase price, though this varies by market. In competitive markets, offering 2–3% signals stronger commitment and can differentiate your offer. Your earnest money goes toward your down payment and closing costs if the deal closes, so it’s not additional money—it’s money you’d be spending anyway.

Can I make an offer on a house without a pre-approval letter?

Technically yes, but most listing agents won’t take it seriously. A pre-approval letter shows you’ve been vetted by a lender and can actually afford the property. Without one, your offer goes to the bottom of the pile—or straight into the reject folder. Get pre-approved before you start touring homes.

What happens if my offer is rejected—can I submit another one?

Absolutely. A rejection isn’t the end of the road. Ask your agent why it was rejected and adjust accordingly. Sometimes the seller counters, which means they’re interested but want different terms. In multiple-offer situations, the listing agent may invite you to submit a “best and final” offer, giving you a second chance.

Should I waive the home inspection to make my offer more competitive?

I strongly advise against waiving the inspection entirely. It’s the single most important protection a buyer has. Instead, shorten the inspection timeline to 5–7 days and offer to waive minor repair requests under a certain dollar threshold (say, $500–$1,000). This shows flexibility without exposing you to major hidden problems.

How long does a seller have to respond to my purchase offer?

There’s no universal rule—the response timeline is typically specified in your offer and varies by state. Most offers include a 24–72 hour response deadline. In competitive situations with set offer review dates, the seller reviews all offers at once and responds to the winner. Your agent should clarify the expected timeline with the listing agent before you submit.

Your Next Move Matters More Than Your Last Search

The home search gets all the attention. The open houses, the Zillow scrolling at midnight, the neighborhood drive-bys. But the offer is where homeownership is actually won or lost.

If you take one thing from this article, let it be this: treat your offer as a strategic document, not just a form to fill out. Research the seller, analyze the comps, tighten your contingencies, strengthen your earnest money, and present a clean, professional package. The S.O.L.I.D. framework isn’t complicated, but it requires intention.

And if you lose one? That’s okay. The right house will come. I’ve seen buyers go through six rejected offers before landing a home they loved even more than the ones they lost. The framework doesn’t guarantee a win every time, but it guarantees you’re putting your best offer forward—and that’s all you can control.

George is a digital growth strategist and the driving force behind Business Ranker, a platform dedicated to helping businesses improve their online visibility and search engine rankings. With a strong understanding of SEO, content strategy, and data-driven marketing, George works closely with brands to turn traffic into real, measurable growth.